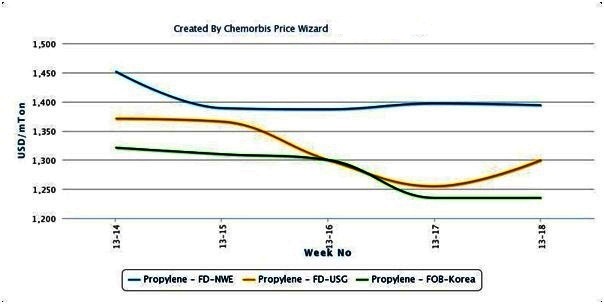

Spot styrene prices in Asia have been steadily rising since the beginning of September on the back of surging energy and benzene costs, as per the pricing service of ChemOrbis. Soaring costs along with benzene and styrene shortages have forced an increasing number of regional PS producers to lower their operating rates recently.

October crude oil delivery contracts on the NYMEX settled at $99/barrel after touching $100/barrel during day trading on Friday, sending the crude oil prices on the NYMEX to their highest level since early May. Stronger crude oil prices have been driving increases in spot benzene prices since early September. In Asia, spot benzene prices have posted a cumulative increase of $90/ton on an FOB South Korea basis since the beginning of September.

Rising benzene values triggered significant increases in spot styrene prices. Limited styrene availability due to some ongoing shutdowns in the region also pushed spot prices higher. Spot styrene prices spiked $85/ton on an FOB South Korea basis week over week. Spot styrene prices have posted a cumulative increase of around $130/ton with respect to early September.

In response to persistently surging production costs, a number of Asian PS producers have started to run their plants at lower rates this week. These producers cited their losses stemming from higher styrene prices as the main reason behind their reduced rates.

Chinese B-grade PS producer Zhanjiang New Zhongmei Chemical reduced the operating rates of its plants from 80-90% to 70-80% over the past week. A company source reported, “We had to cut our production rates to avoid greater loss given higher styrene prices versus the relatively smaller hikes attainable on GPPS and HIPS prices.”

A source from SK Networks Shantou Polystyrene Resin, another B-grade PS producer in China, reported that they shut their GPPS line in late August due to soaring styrene prices. The company is not offering GPPS for now and their expected restart date has not been disclosed. Meanwhile, their two HIPS lines are running at below normal rates of around 60% of capacity.

We have not been able to reflect higher styrene costs onto our HIPS prices for the moment and therefore we are running our lines at lower rates than normal,” the source told ChemOrbis. The company can produce 150,000 tons of material through their one GPPS and two HIPS lines, with each line having approximately 50,000 tons/year of capacity.

A Taiwanese producer, Kaofu, had previously lowered operating rates at their GPPS and HIPS lines to 70%, with a company source reporting that they cut their operating rates again last week citing their lack of sufficient styrene availability. The company can produce 50,000 tons/year of both GPPS and HIPS at their facility.

Another producer in Taiwan, Grand Pacific Petrochemical Corporation, reduced their production rates to less than 70-80% at their HIPS and ABS lines last week. The company also cut operating rates at its 330,000 tons/year styrene plant to 85-90% owing to a benzene shortage. Additionally, Korea Kumho Petrochemicals is planning to shut their ABS and PS plants in October for a two week long maintenance. “We are already suffering losses on our ABS business due to firmer styrene costs,” a company source lamented.

{kind=link}